The

Matching Principle

-

How the Matching Principle Works

-

Why It Matters

-

Matching vs. Cash Timing

The Matching Principle

The Matching Principle is a

fundamental rule in accrual accounting. It ensures that expenses are

recorded in the same period as the revenues they helped generate.

"The Matching Principle states that businesses must match expenses to the revenue they helped earn—regardless of when the cash is paid.”

This concept helps paint a more accurate and fair picture of business performance.

"The Matching Principle states that businesses must match expenses to the revenue they helped earn—regardless of when the cash is paid.”

This concept helps paint a more accurate and fair picture of business performance.

1. How the Matching Principle Works

Imagine you run a bakery. You sell

1,000 cupcakes in June, earning $3,000 in revenue. You also bought flour and

paid employees that month to make the cupcakes. Even if you pay your suppliers

in July, those costs are matched to June, because that’s when the income

was earned.

This keeps your Income Statement clean and consistent—linking income with the costs that made it possible.

This keeps your Income Statement clean and consistent—linking income with the costs that made it possible.

2. Why It Matters

Without the matching principle,

a business might record income in one month and the related expenses in

another, leading to distorted profit figures that don’t reflect the true

financial performance. This makes it harder to understand how well the business

is actually doing. The matching principle ensures that financial reports are accurate,

consistent, and useful for decision-making. It is especially

important for businesses that provide services, manufacture products, or manage

payroll and inventory, where timing plays a key role in financial clarity.

3. Matching vs. Cash Timing

This principle does not follow when

the cash leaves the bank—it follows when the expense actually helps generate

income. That’s why it’s only used in accrual accounting, not

cash-based systems.

Key Takeaways

✅ Match expenses to the revenue they helped earn

✅ This principle ensures financial reports reflect true performance

✅ It’s a core part of accrual accounting (not cash accounting)

✅ Matching improves accuracy and consistency in the Income Statement

✅ It helps businesses make smarter decisions based on real results

✅ This principle ensures financial reports reflect true performance

✅ It’s a core part of accrual accounting (not cash accounting)

✅ Matching improves accuracy and consistency in the Income Statement

✅ It helps businesses make smarter decisions based on real results

Write your awesome label here.

Access all Accounting and Bookkeeping Courses from One Portal.

Mastering Bookkeeping and Accounting

MBA simplifies accounting, ledger management, account balancing and financial statement preparation.

QuickBooks Online For Bookkeepers

From Beginner to Expert: Master QuickBooks Online. Effortlessly Navigate, Analyze Transactions, and Unlock its Full Potential.

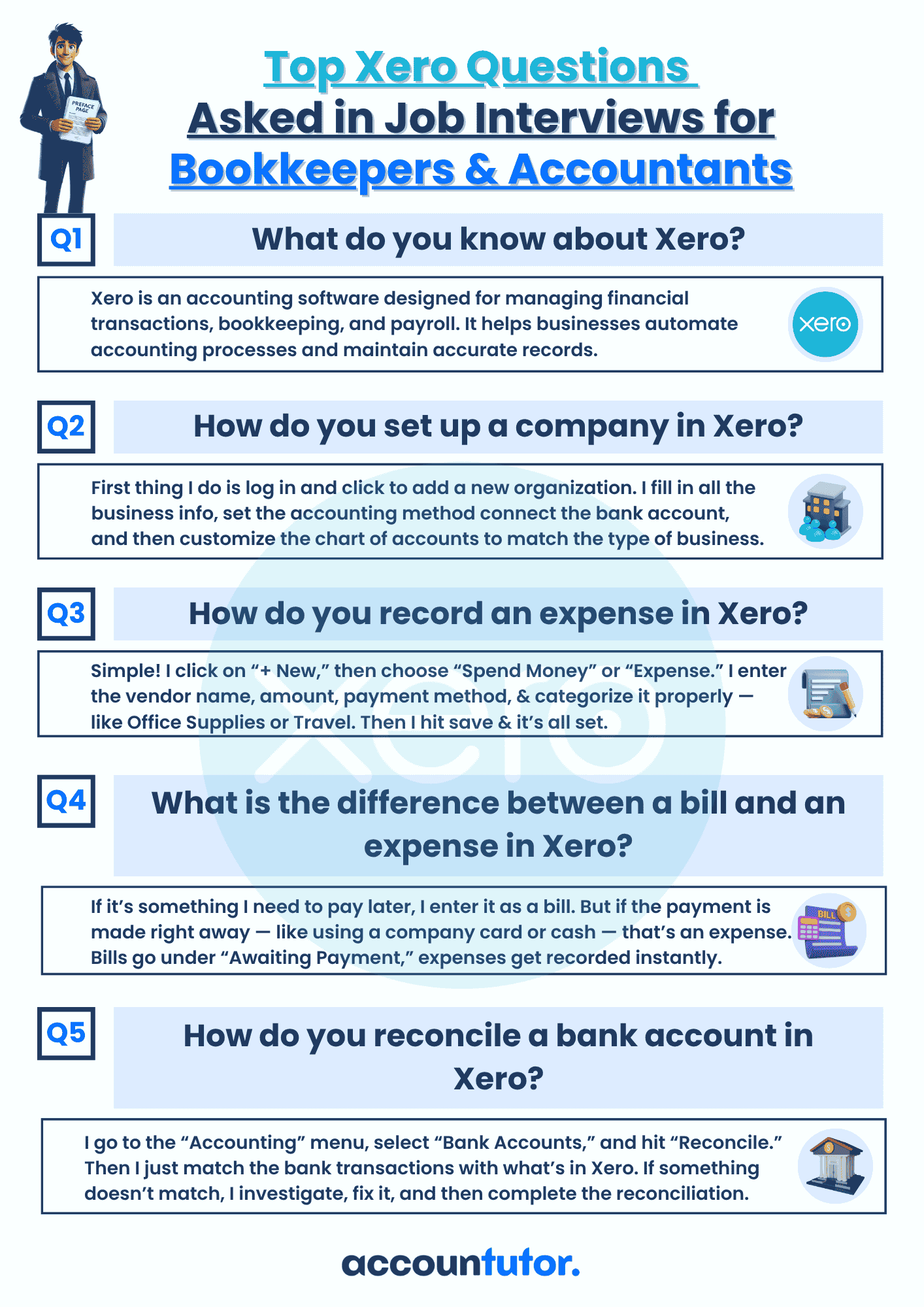

Xero Accounting For Bookkeepers

Learn how to use Xero, the leading online accounting software to perform most of the essential bookkeeping tasks.

ChatGpt for Bookkeepers and Accountants

Learn how to use the ChatGPT prompt toolkit to simplify daily accounting tasks for accountants and bookkeepers instantly.

Subscribe to our newsletter

Stay informed with the latest accounting tips, tools, and updates from Accountutor right in your email inbox.

Thank you!

Policy Pages

Download QuickBooks Online PDF Guide

Thank you!

Download QuickBooks Online Cheat Sheet

Thank you!

Download ABCD of Accounting

Thank you!

Download Checklist 2024

Thank you!

Register For Free!

Thank you!

Download Interview Questions

Thank you!

Register for this webinar: How to Master QuickBooks Online— Without Feeling Overwhelmed

7th JUNE 2025 | 8:00 AM PST | 11:00 AM EST

Thank you! The joining link will be sent to your email shortly!

Webinar joining link will be sent to your email address.

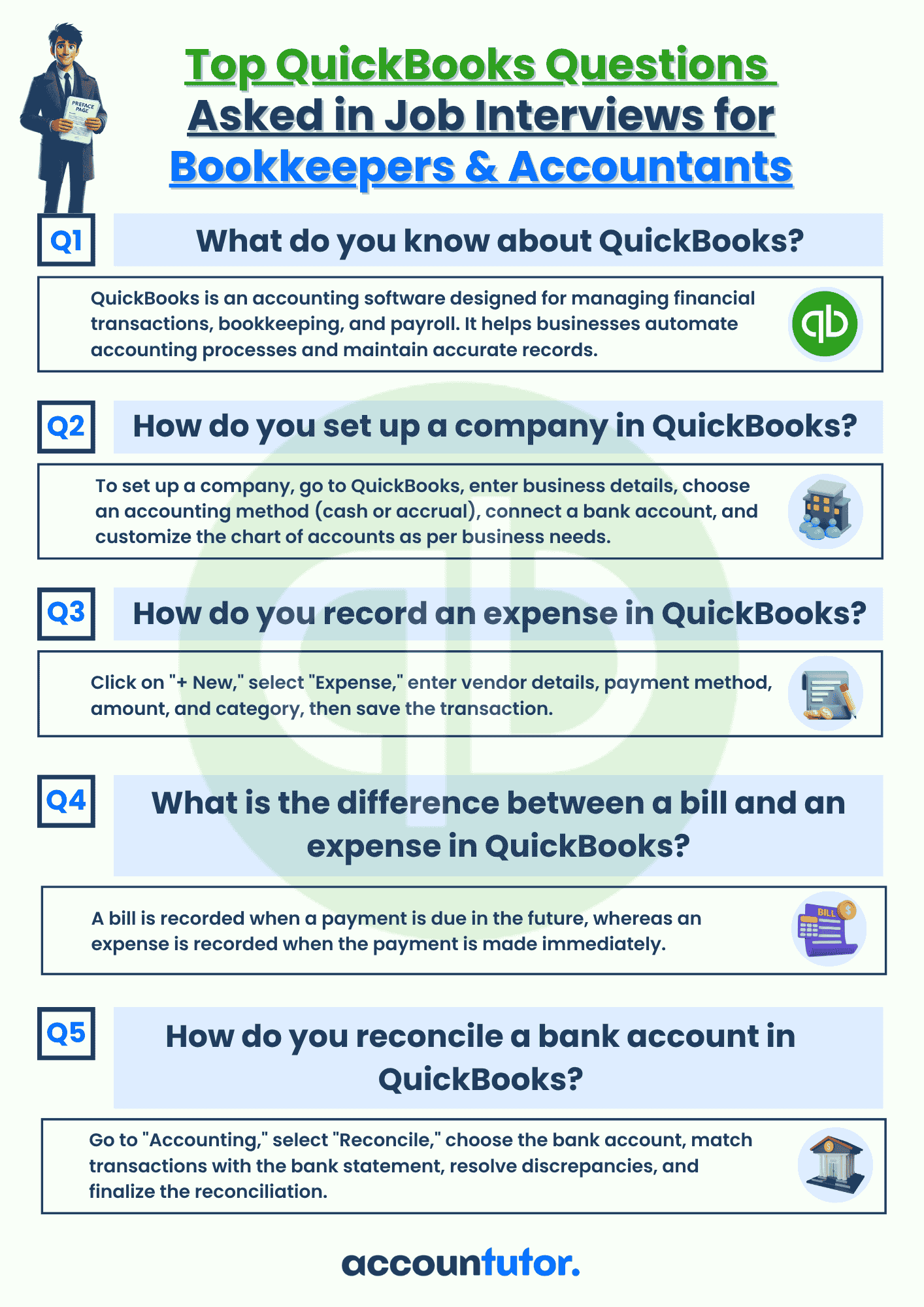

Download QBO Job Interview Questions and Answers PDF

Thank you!

Download Interview Questions

Thank you!

Download 50 Interview Questions For Bookkeepers

Thank you!

Download QuickBooks Online Guidebook

Thank you!

Created with