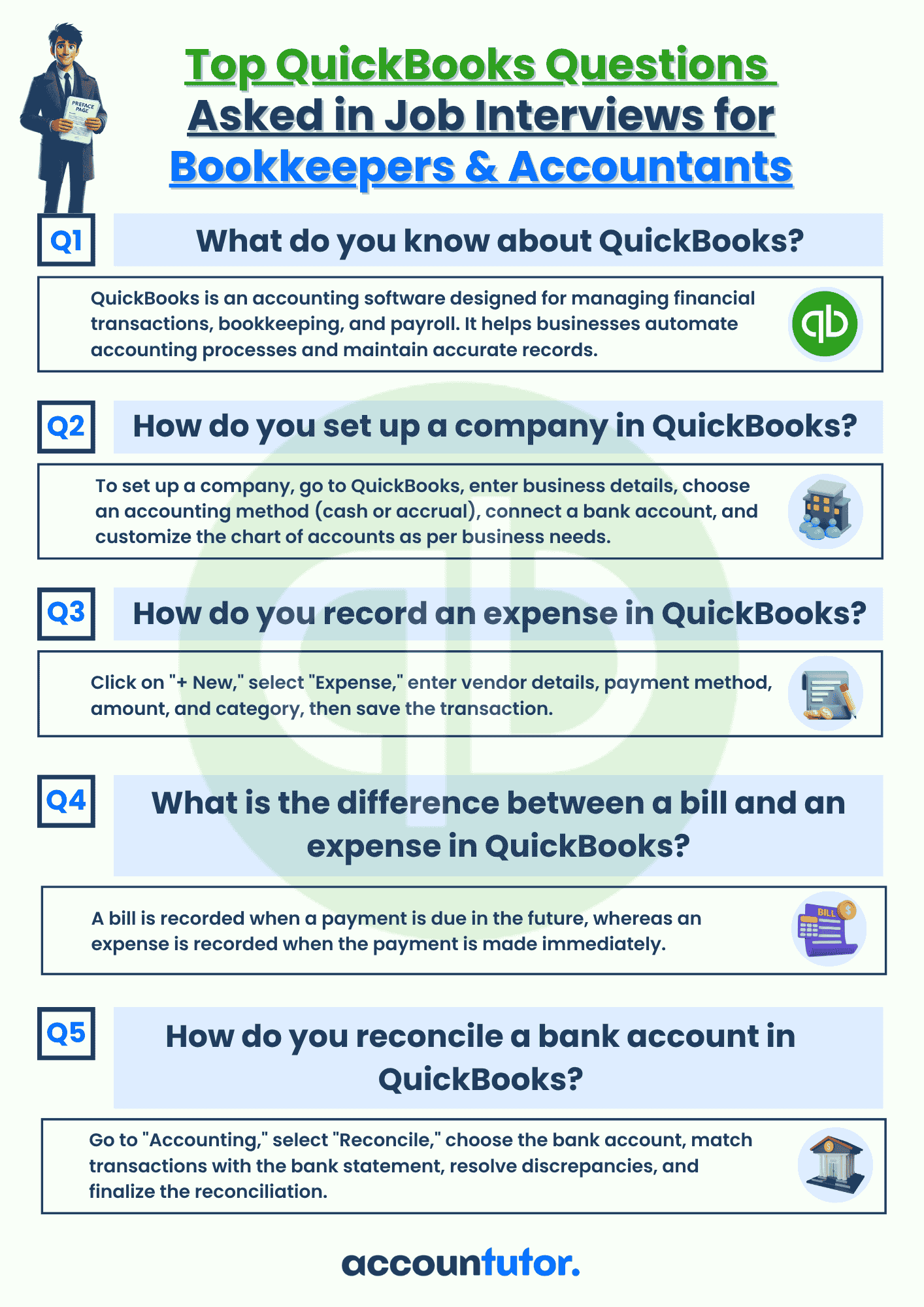

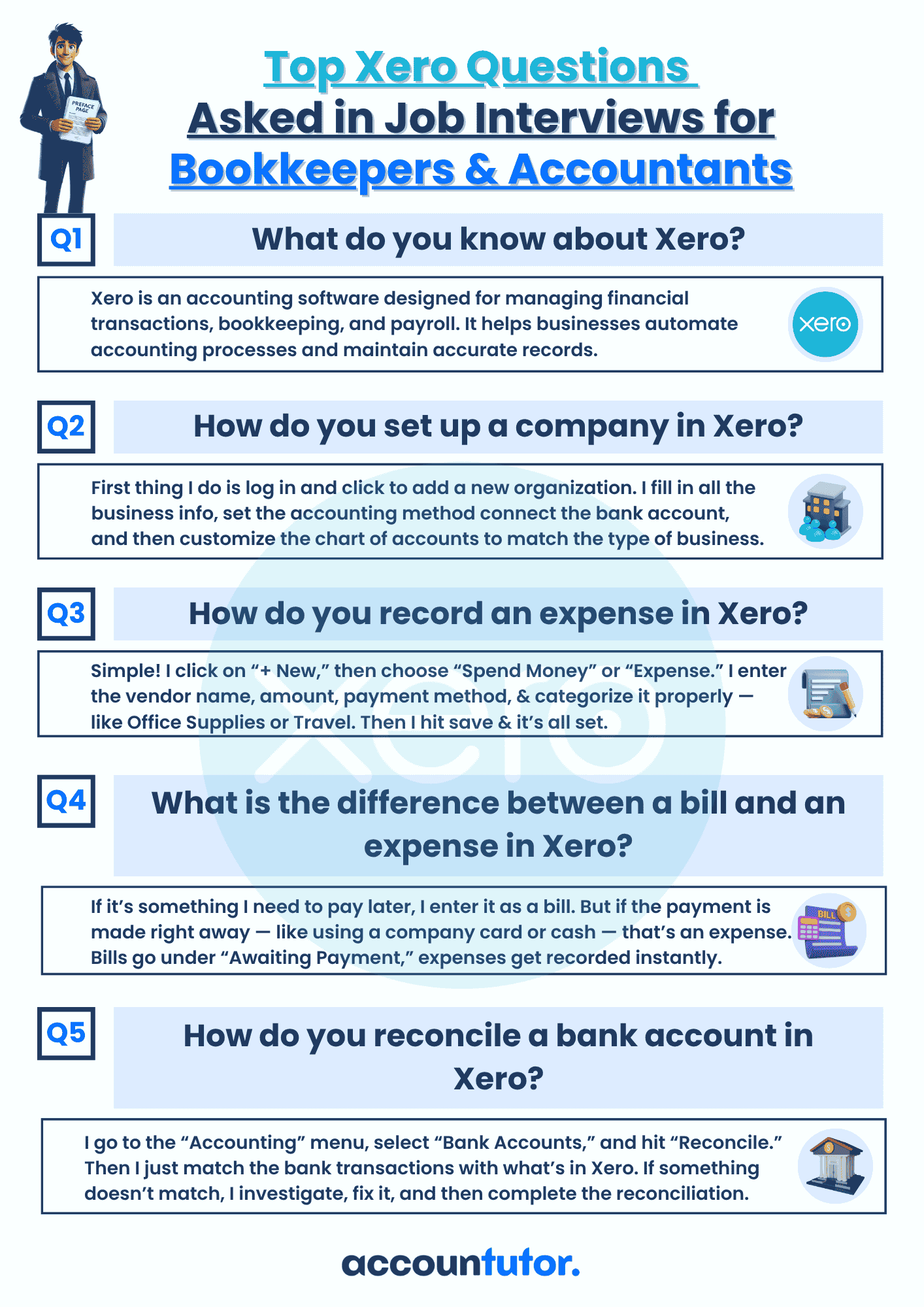

Steps

in Reconciling Bank Statements

-

Get Your Records Ready

-

Match Each Transaction

-

Check for Outstanding Items

-

Identify Bank Charges or Interest

-

Fix Any Errors

-

Confirm the Final Balance

Steps in Reconciling Bank Statements

Bank reconciliation isn’t just a good habit—it’s a step-by-step process that

helps you confirm your financial records are accurate. According to bookkeeping

practice:

“Bank reconciliation involves comparing the transactions in your accounting records to those listed in your bank statement and identifying any differences.”

Let’s walk through the process in simple, beginner-friendly steps.

“Bank reconciliation involves comparing the transactions in your accounting records to those listed in your bank statement and identifying any differences.”

Let’s walk through the process in simple, beginner-friendly steps.

1. Get Your Records Ready

Start by gathering your bank

statement for the period you want to reconcile—usually a month. Then, open

your business’s cash book or accounting software. These are the two

documents you’ll compare.

2. Match Each Transaction

Go line by line and match every deposit,

withdrawal, payment, or fee on the bank statement with the

ones in your records. Check that the dates, amounts, and descriptions

match. If something appears on one but not the other, flag it for review.

3. Check for Outstanding Items

Sometimes, you’ve recorded a

transaction in your books, but it hasn’t cleared the bank yet. These are called

outstanding items—like uncashed checks or recent deposits. Make a note

of these so they don’t throw off your reconciliation.

4. Identify Bank Charges or Interest

Banks often charge service fees or

add interest that you might not have recorded yet. Add these missing items

to your records so your balance reflects the true picture.

5. Fix Any Errors

If you find typos, double entries,

or forgotten transactions—correct them in your records. The goal is to

adjust your books so they match the bank statement exactly (apart from any

outstanding items, which will clear next month).

6. Confirm the Final Balance

After matching and adjusting

everything, compare your adjusted book balance to the bank

statement’s ending balance. If they match—great! Your reconciliation is

complete.

Key Takeaways

✅ Start with your bank statement and your accounting records

side by side

✅ Match each transaction and flag differences

✅ Identify outstanding checks or deposits not yet processed

✅ Record missing charges like bank fees or interest

✅ Fix errors to make sure your books and bank statement agree

✅Once balanced, you can confidently close the books for that period

✅ Match each transaction and flag differences

✅ Identify outstanding checks or deposits not yet processed

✅ Record missing charges like bank fees or interest

✅ Fix errors to make sure your books and bank statement agree

✅Once balanced, you can confidently close the books for that period

Write your awesome label here.

Access all Accounting and Bookkeeping Courses from One Portal.

Mastering Bookkeeping and Accounting

MBA simplifies accounting, ledger management, account balancing and financial statement preparation.

QuickBooks Online For Bookkeepers

From Beginner to Expert: Master QuickBooks Online. Effortlessly Navigate, Analyze Transactions, and Unlock its Full Potential.

Xero Accounting For Bookkeepers

Learn how to use Xero, the leading online accounting software to perform most of the essential bookkeeping tasks.

ChatGpt for Bookkeepers and Accountants

Learn how to use the ChatGPT prompt toolkit to simplify daily accounting tasks for accountants and bookkeepers instantly.

Subscribe to our newsletter

Stay informed with the latest accounting tips, tools, and updates from Accountutor right in your email inbox.

Thank you!

Policy Pages

Download QuickBooks Online PDF Guide

Thank you!

Download QuickBooks Online Cheat Sheet

Thank you!

Download ABCD of Accounting

Thank you!

Download Checklist 2024

Thank you!

Register For Free!

Thank you!

Download Interview Questions

Thank you!

Register for this webinar: How to Master QuickBooks Online— Without Feeling Overwhelmed

7th JUNE 2025 | 8:00 AM PST | 11:00 AM EST

Thank you! The joining link will be sent to your email shortly!

Webinar joining link will be sent to your email address.

Download QBO Job Interview Questions and Answers PDF

Thank you!

Download Interview Questions

Thank you!

Download 50 Interview Questions For Bookkeepers

Thank you!

Download QuickBooks Online Guidebook

Thank you!

Created with