Common

Bookkeeping Accounts

-

Asset Accounts

-

Liability Accounts

-

Equity Accounts

-

Income Accounts

-

Expense Accounts

Common

Bookkeeping Accounts

Bookkeeping involves tracking all

the financial activities of a business, and to do that effectively, you need to

understand the most common accounts used in the Chart of Accounts. These

accounts help categorize income, expenses, assets, liabilities, and equity in a

way that makes financial reports accurate and meaningful.

“Bookkeeping accounts are specific categories used to organize financial transactions for proper recording and reporting.”

Let’s explore the main types of accounts that appear in almost every business.

“Bookkeeping accounts are specific categories used to organize financial transactions for proper recording and reporting.”

Let’s explore the main types of accounts that appear in almost every business.

1. What Is the General Ledger?

Asset accounts track what the business

owns. Common examples include cash, which

represents money in hand or in bank accounts, and accounts receivable, which is

the money customers owe to the business. Inventory

refers to goods available for sale, while prepaid

expenses include payments made in advance, such as insurance.

Other asset accounts may include equipment or furniture,

which are physical items used in the daily operations of the business. These

accounts increase when the business acquires something of value and decrease

when those assets are either used or sold.

2. Posting Entries to the General Ledger

Liability accounts represent what the

business owes to others. Common examples include accounts payable, which refers

to unpaid bills to suppliers, and loans payable,

which are outstanding amounts borrowed from banks or other lenders. Taxes payable covers taxes that

are due but haven’t been paid yet, while wages payable

represents salaries earned by employees that are still unpaid. These

liabilities increase when the business borrows money or delays payment, and

they decrease when those debts or obligations are settled.

3. Equity Accounts

Equity accounts show the owner’s claim or

stake in the business. These accounts reflect how much of the business truly

belongs to the owner after all debts are paid. Examples include Owner’s Capital, which is the

money the owner invests into the business, Owner’s

Drawings, which represents money withdrawn by the owner for

personal use, and Retained Earnings,

which are profits that are kept in the business rather than distributed. Equity

increases when the owner adds more funds or when the business earns a profit,

and it decreases when there are losses or when the owner takes money out of the

business.

4. Income Accounts

Income accounts, also known as revenue accounts, track the money a

business earns through its operations. Common examples include Sales Revenue, which is income

generated from selling products, Service Income,

which refers to money earned by providing services, and Interest Income, which includes

earnings from bank interest or other investments. These accounts increase as

the business brings in more revenue and serve as a key indicator of how well

the business is performing financially.

5. Expense Accounts

Expense

accounts show what the business spends to keep its operations running

smoothly. Some of the most common

expense accounts include Rent Expense, which covers the cost of office

or shop space, and Utilities Expense, which includes electricity, water,

internet, and other essential services. Salaries or Wages Expense

reflects the money paid to employees, while Office Supplies Expense

tracks spending on items like pens, paper, and software. Advertising Expense

covers marketing and promotional efforts to attract customers. These accounts

increase whenever the business incurs a cost and play a crucial role in

tracking where money is going and managing overall spending.

Key Takeaways

✅ Bookkeeping accounts help organize financial transactions for accurate recording and reporting

✅ Asset accounts track what the business owns—like cash, inventory, and equipment

✅ Liability accounts show what the business owes—such as loans, payables, and taxes

✅ Equity accounts represent the owner’s claim—capital invested, drawings, and retained earnings

✅ Income accounts record money earned from sales, services, or interest

✅ Asset accounts track what the business owns—like cash, inventory, and equipment

✅ Liability accounts show what the business owes—such as loans, payables, and taxes

✅ Equity accounts represent the owner’s claim—capital invested, drawings, and retained earnings

✅ Income accounts record money earned from sales, services, or interest

Write your awesome label here.

Access all Accounting and Bookkeeping Courses from One Portal.

Mastering Bookkeeping and Accounting

MBA simplifies accounting, ledger management, account balancing and financial statement preparation.

QuickBooks Online For Bookkeepers

From Beginner to Expert: Master QuickBooks Online. Effortlessly Navigate, Analyze Transactions, and Unlock its Full Potential.

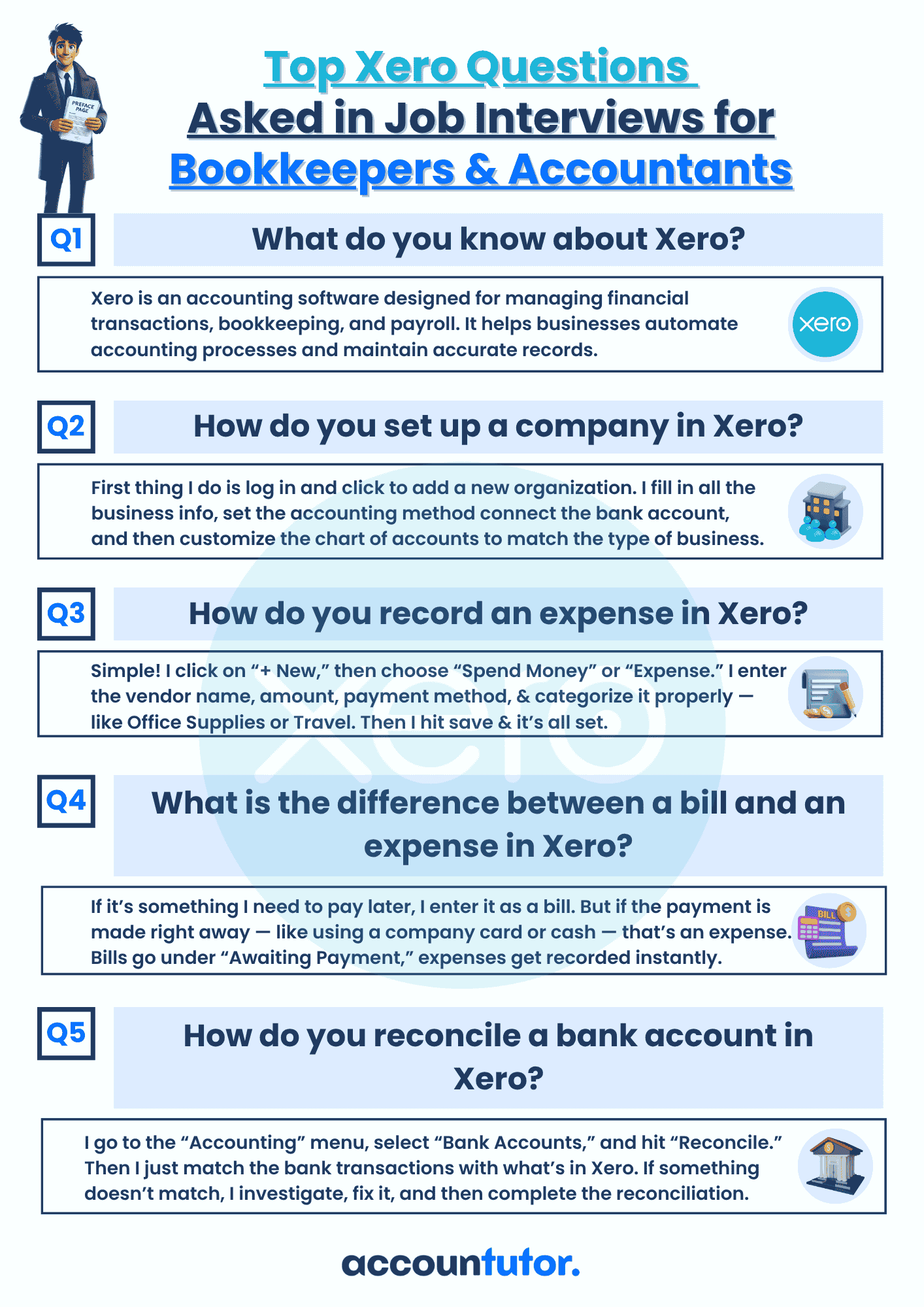

Xero Accounting For Bookkeepers

Learn how to use Xero, the leading online accounting software to perform most of the essential bookkeeping tasks.

ChatGpt for Bookkeepers and Accountants

Learn how to use the ChatGPT prompt toolkit to simplify daily accounting tasks for accountants and bookkeepers instantly.

Subscribe to our newsletter

Stay informed with the latest accounting tips, tools, and updates from Accountutor right in your email inbox.

Thank you!

Policy Pages

Download QuickBooks Online PDF Guide

Thank you!

Download QuickBooks Online Cheat Sheet

Thank you!

Download ABCD of Accounting

Thank you!

Download Checklist 2024

Thank you!

Register For Free!

Thank you!

Download Interview Questions

Thank you!

Register for this webinar: How to Master QuickBooks Online— Without Feeling Overwhelmed

7th JUNE 2025 | 8:00 AM PST | 11:00 AM EST

Thank you! The joining link will be sent to your email shortly!

Webinar joining link will be sent to your email address.

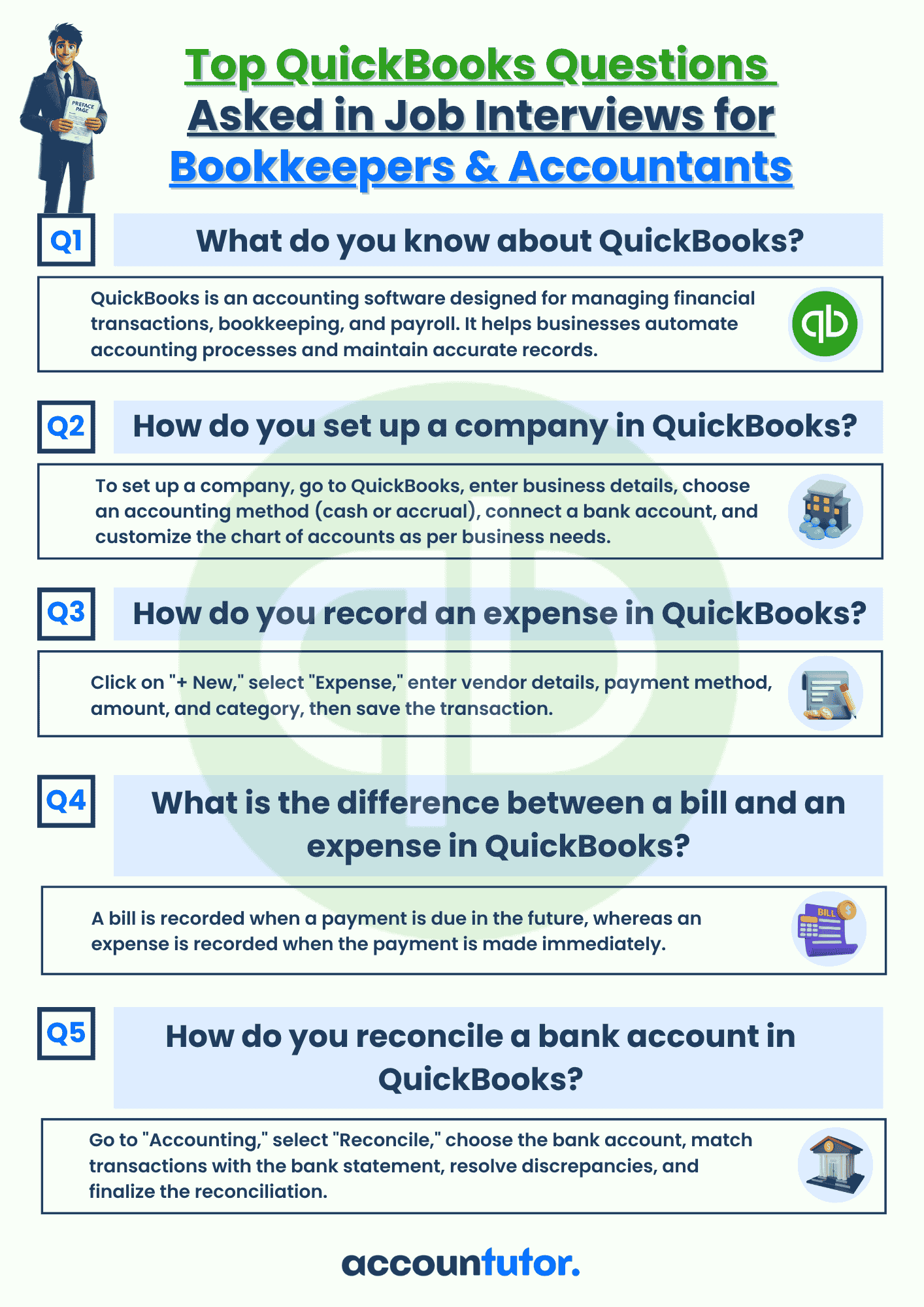

Download QBO Job Interview Questions and Answers PDF

Thank you!

Download Interview Questions

Thank you!

Download 50 Interview Questions For Bookkeepers

Thank you!

Download QuickBooks Online Guidebook

Thank you!

Created with