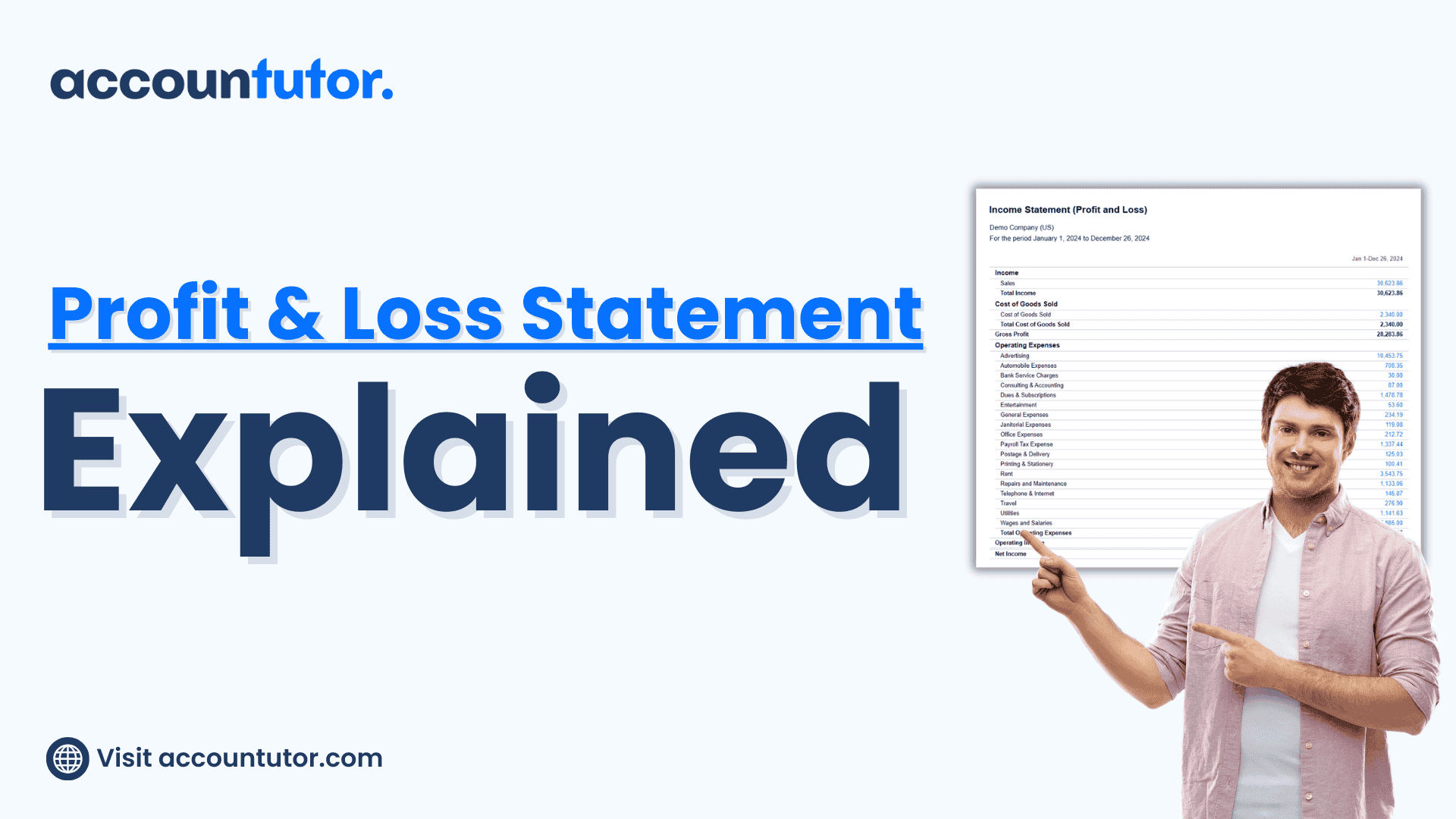

What is Profit and Loss Statement?

What is the Profit and Loss Account, and Why is it Essential for Business Success?

At its core, the Profit and Loss Account has two main sections:

- Income: Captures all revenue earned during the period.

- Expenses: Tracks all costs associated with generating that income.

By subtracting total expenses from total income, you arrive at the net profit or loss, giving you a clear picture of your business's financial health. This document is not just about numbers—it’s about the story of your business’s performance and the insights needed to make informed decisions.

Breaking Down the Income Section

- A café’s sales from coffee, pastries, and other menu items.

- A retailer’s revenue from selling products.

- A service provider’s earnings from fees or subscriptions.

Accrual Accounting and Income Recognition

Income is typically recognized when it’s earned, not necessarily when the cash is received. This practice, known as accrual accounting, ensures that financial statements reflect the true performance of the business.

Example: A bakery sells cakes to a local restaurant on credit. The revenue from the sale is recorded when the cakes are delivered, even though payment might be received a month later.

Why This Matters: Accrual accounting aligns income with the expenses incurred to generate it, providing a more accurate and reliable picture of profitability.

Understanding the Expenses Section

1. Cost of Goods Sold (COGS):

COGS represents the direct costs involved in producing or purchasing the goods your business sells.

Examples of COGS:

For a bakery: Flour, sugar, and labor costs associated with baking pastries.

For a clothing store: The cost of purchasing inventory from suppliers.

COGS is a critical figure because it directly impacts gross profit, which is calculated as: Gross Profit=Income−COGS

Example:

A bakery earns $15,000 from sales in a month. If the COGS is $4,000, the gross profit is:

$15,000−$4,000=$11,000

2. Operating Expenses

Operating expenses include the costs required to keep the business running but are not directly tied to the production of goods or services.

Examples of Operating Expenses:

Rent: For office or retail

space.

Utilities: Electricity,

water, and internet.

Salaries: For employees

not involved in production, such as administrative staff.

Marketing: Advertising and

promotional costs.

These expenses are necessary for day-to-day operations and can significantly impact net profit.

3. Non-Operating Expenses

Non-operating expenses are costs not related to the core business activities. These might include:

Interest Payments: On loans or other borrowed funds.

Losses from Investments: Declines in the value of financial investments.

While these expenses don’t reflect the business’s main operations, they still affect overall profitability and should be monitored carefully.

Putting It All Together: A Simple Example

Monthly Income:

Expenses:

COGS: Flour, sugar, and labor: $4,000

Operating Expenses:

- Rent: $1,000

- Salaries: $3,000

- Utilities: $500

- Marketing: $500

Total Expenses: $4,000 (COGS)+$1,000 (Rent)+$3,000 (Salaries)+$500 (Utilities)+$500 (Marketing)=$9,000

Net Profit:

$15,000−$9,000

$6000

In this example, the bakery’s Profit and Loss Account reveals a net profit of $6,000 for the month.

Why the Profit and Loss Account Matters

1. Measuring Profitability

By calculating net profit or loss, the P&L Account shows whether the business is making or losing money during a specific period. This insight is critical for evaluating success and setting financial goals.

2. Identifying Opportunities

The detailed breakdown of income and expenses helps businesses: Spot areas where costs can be reduced. Identify products or services that generate the most revenue.

Example: If marketing expenses are high but not driving significant sales, the business might adjust its strategy to focus on more cost-effective campaigns.

3. Informed Decision-Making

With accurate financial data, business owners can make smarter decisions, such as:

- Adjusting pricing strategies.

- Allocating resources more effectively.

- Planning for expansion or investment.

4. Ensuring Financial Control

Regularly reviewing the Profit and Loss Account keeps businesses in control of their finances, helping them avoid cash flow problems and stay on track for long-term success.

Common Mistakes in Managing

the Profit and Loss Account

1.Failing to Include All Expenses: Overlooking small costs, such as office supplies or software subscriptions, can lead to inaccurate financial reports.

2.Misclassifying Expenses: Incorrectly categorizing expenses (e.g., recording marketing costs as COGS) can distort profitability figures.

3.Neglecting Regular Reviews: Reviewing the P&L Account only annually or sporadically can result in missed opportunities to address financial issues promptly.

Practical Tips for Managing Your Profit and Loss Account

2. Review Monthly: Regular reviews allow you to track performance, identify trends, and make timely adjustments.

3. Consult Professionals: For complex financial situations, seek advice from accountants or financial consultants.

Take Your Accounting Knowledge to the Next Level

Understanding the Profit and Loss Account is a vital skill for business success. But it’s just the beginning. To dive deeper into accounting concepts and become more confident in managing your finances, enroll in our free mini-course, ‘Accounting Explained,’ on Accountutor.com.

Our expert-led courses simplify accounting for bookkeepers, small business owners, and anyone interested in mastering financial management. With practical examples and hands-on tutorials, you’ll learn to manage financial statements, make smarter decisions, and grow your business with ease.

Visit Accountutor.com today and take control of your financial future!

Conclusion

The Profit and Loss Account is a window into your business’s financial

performance, showing how income and expenses impact profitability. By breaking

down revenue, COGS, operating expenses, and non-operating costs, this statement

provides actionable insights that drive smarter decision-making.

Whether you’re a small business owner or an aspiring accountant, mastering

the Profit and Loss Account empowers you to manage finances effectively,

identify opportunities, and achieve long-term success.

Start your journey today with Accountutor’s free resources and courses. Visit Accountutor.com now and transform the way you understand and manage your business’s finances!

Subscribe to our newsletter

Policy Pages

Register for this webinar: How to Master QuickBooks Online— Without Feeling Overwhelmed