What is Cost of Goods Sold (COGS)?

Dec 25

Introduction

Cost of Goods Sold (COGS) represents the direct costs incurred in producing goods or services that a business sells during a specific period. It includes expenses such as raw materials, labor, and manufacturing overhead directly attributable to production. COGS is a critical figure in determining a company’s gross profit, calculated as:

Gross Profit = Revenue - COGS.

COGS provides insight into the efficiency of production processes and the profitability of sales.

How it works?

A bakery sells 5,000 loaves of bread in June for $20,000. To produce these loaves, the bakery incurs $6,000 for flour, yeast, and other ingredients, $4,000 for labor, and $2,000 in utilities for running ovens and maintaining storage. The total COGS for June is $12,000. By subtracting COGS from the $20,000 revenue, the bakery calculates a gross profit of $8,000, which it uses to cover operating expenses like rent and marketing. This analysis helps the bakery assess the efficiency of its production costs relative to its sales.

Why it is important?

COGS is a vital financial metric for businesses as it impacts profitability, pricing strategies, and financial reporting. Here’s why it is essential:

1. Profitability Measurement: COGS directly affects gross profit, which is a key indicator of how efficiently a business produces and sells goods.

Example: A clothing retailer analyzes COGS to determine whether its $50,000 gross profit aligns with production efficiency goals.

2. Pricing Strategy: Understanding COGS helps businesses set appropriate selling prices to ensure profitability.

Example: A smartphone manufacturer calculates the COGS per unit to set competitive pricing while maintaining a 30% profit margin.

3. Cost Control: Businesses monitor COGS to identify inefficiencies in production or supply chains, enabling cost reduction.

Example: A furniture company renegotiates supplier contracts to lower raw material costs and improve gross margins.

4. Inventory Valuation: COGS plays a crucial role in inventory management by determining the value of goods sold versus unsold stock.

Example: A grocery store calculates the COGS for perishables sold to assess the profitability of its inventory turnover.

Types of Costs in COGS:

1. Direct Materials: Direct materials are the raw materials or components that become a part of the finished product. These materials are directly traceable to the production of goods and form a significant portion of COGS.

Example: A furniture manufacturer includes the cost of wood, nails, and varnish as direct materials since these are integral to producing tables and chairs.

2. Direct Labor: Direct labor refers to the wages paid to employees who are directly involved in the production process. These workers’ efforts can be specifically traced to creating the product.

Example: A bakery records the wages paid to bakers who mix ingredients and operate ovens as direct labor costs.

3. Manufacturing Overhead: Manufacturing overhead includes indirect costs related to the production process that cannot be directly traced to a specific product. This includes factory utilities, equipment depreciation, and factory maintenance.

Example: A shoe factory includes costs like electricity to power machines, cleaning supplies for the factory, and equipment repairs as part of manufacturing overhead.

4. Freight-In Costs: Freight-in costs are the transportation expenses incurred to bring raw materials or inventory to the production facility. These costs are added to the total production cost as they directly impact the availability of materials.

Example: A clothing retailer includes the $3,000 shipping cost for fabric imports in its COGS calculation.

5. Inventory Adjustments: Inventory adjustments consider the beginning inventory, purchases during the period, and ending inventory to calculate the total cost of goods sold. This ensures only the costs related to items sold are accounted for in COGS.

Example: A grocery store starts with $10,000 in inventory, purchases $5,000 worth of goods, and ends with $2,000 in unsold inventory. The COGS is calculated as $10,000 (beginning) + $5,000 (purchases) - $2,000 (ending) = $13,000.

Conclusion:

COGS is a fundamental metric for understanding the relationship between production costs and revenue generation. By carefully analyzing COGS, businesses can evaluate production efficiency, refine pricing strategies, and improve profitability. Accurate tracking of direct materials, labor, and overhead ensures transparent financial reporting and effective cost management, making COGS an indispensable tool for operational and strategic decision-making.

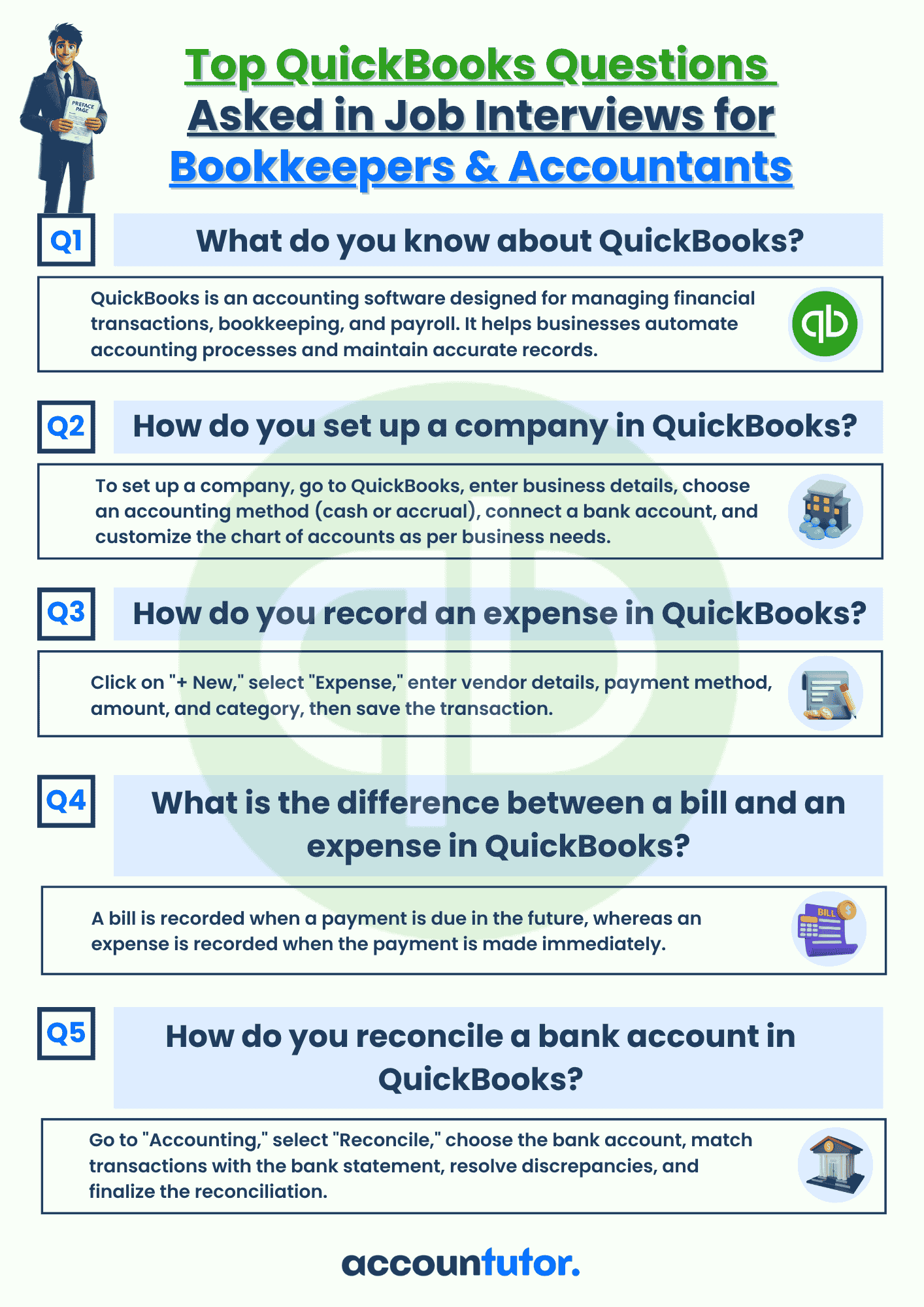

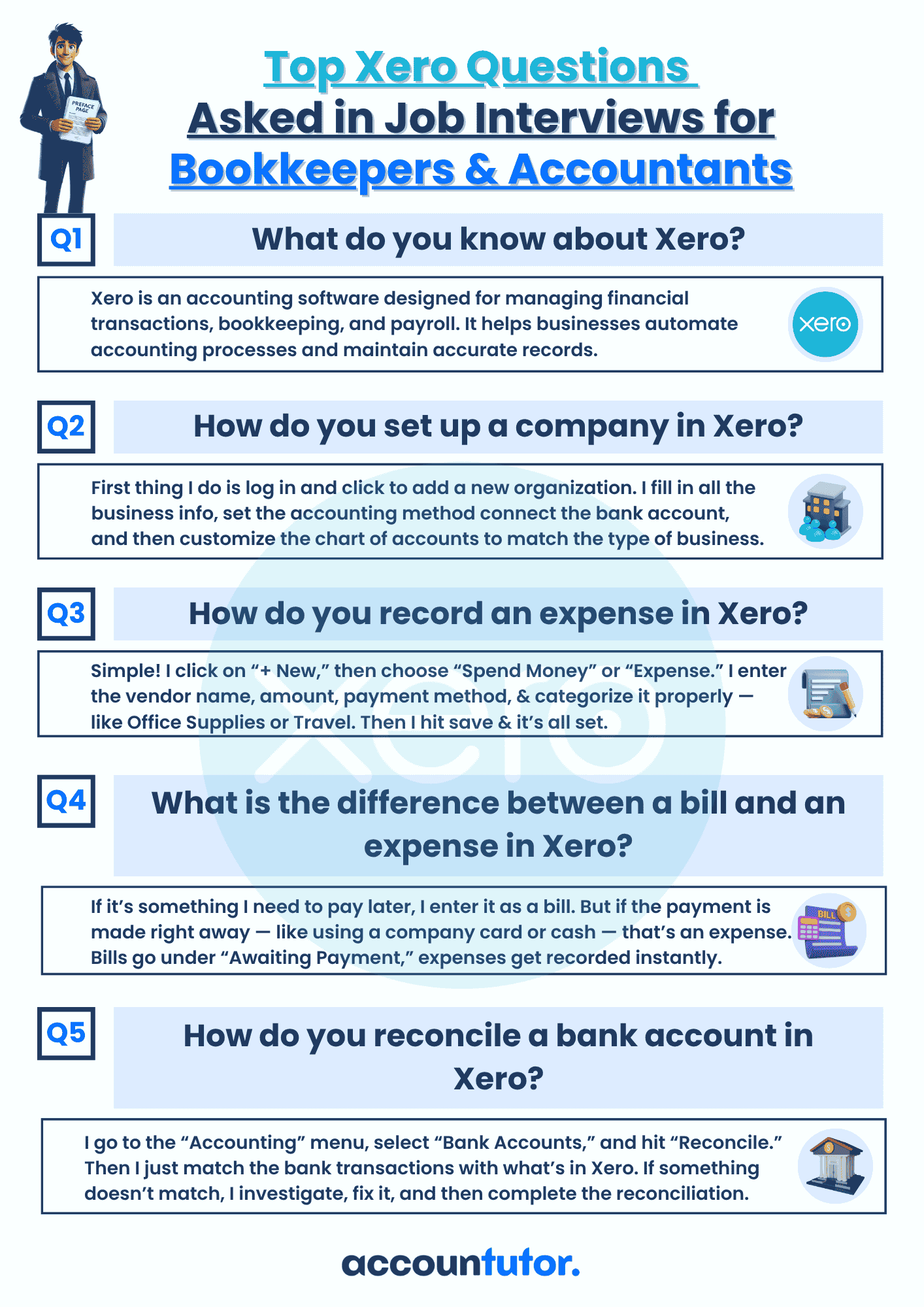

Accounting and Bookkeeping courses for you

Subscribe to our newsletter

Stay informed with the latest accounting tips, tools, and updates from Accountutor right in your email inbox.

Thank you!

Policy Pages

Download QuickBooks Online PDF Guide

Thank you!

Download QuickBooks Online Cheat Sheet

Thank you!

Download ABCD of Accounting

Thank you!

Download Checklist 2024

Thank you!

Register For Free!

Thank you!

Download Interview Questions

Thank you!

Register for this webinar: How to Master QuickBooks Online— Without Feeling Overwhelmed

7th JUNE 2025 | 8:00 AM PST | 11:00 AM EST

Thank you! The joining link will be sent to your email shortly!

Webinar joining link will be sent to your email address.

Download QBO Job Interview Questions and Answers PDF

Thank you!

Download Interview Questions

Thank you!

Download 50 Interview Questions For Bookkeepers

Thank you!

Download QuickBooks Online Guidebook

Thank you!

Created with