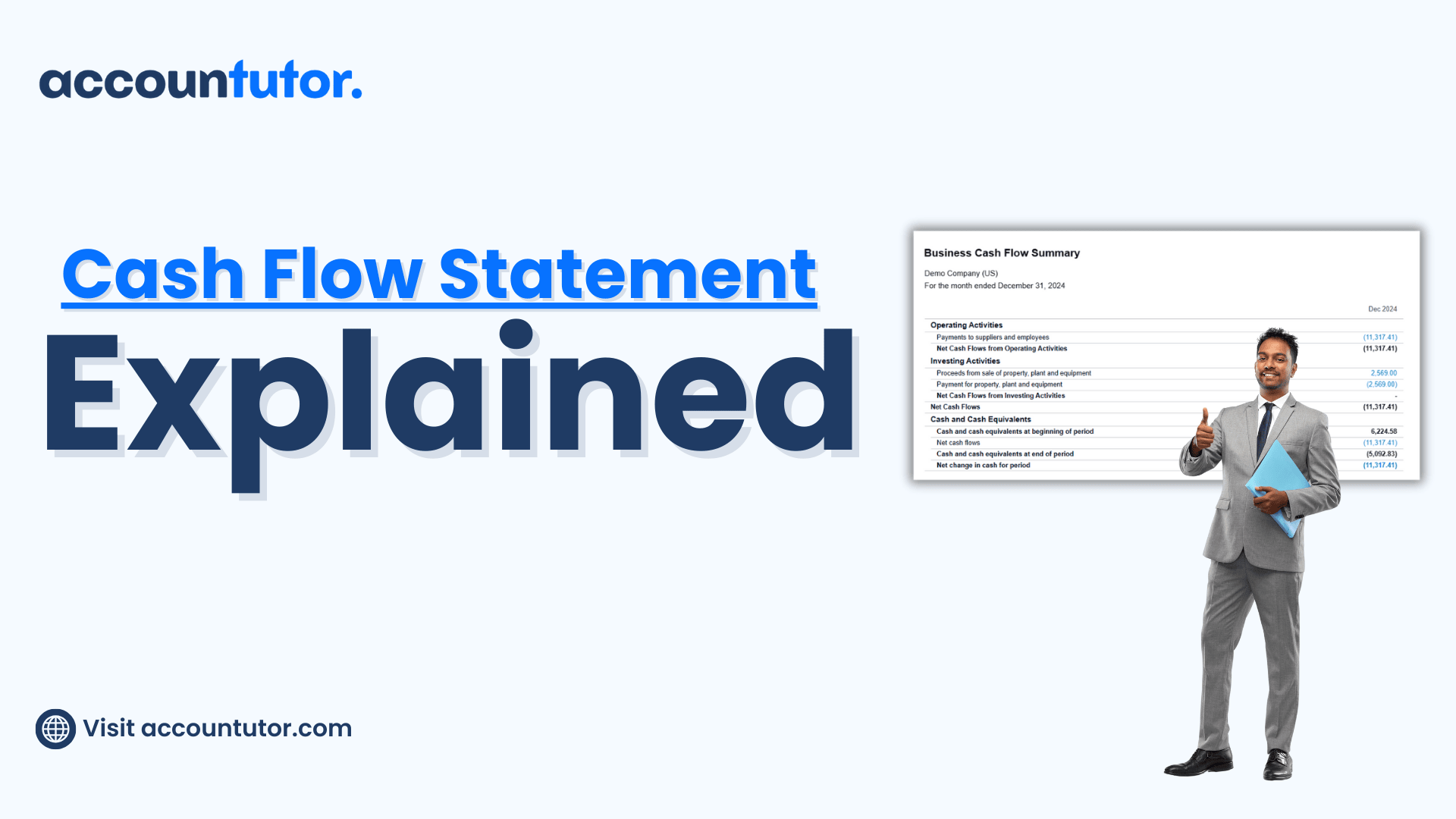

What is Cash Flow Statement?

Mastering the Cash Flow Statement: A Guide for Accountants and Bookkeepers

Have you ever looked at a business’s profits and thought, “Why are we still struggling to pay bills?” If so, this guide is for you. By the time you finish reading, you’ll know exactly how to track and manage your cash flow to keep your business—or your client’s business—financially stabled

What is a Cash Flow Statement?

Why is the Cash Flow Statement Important?

Is there enough cash to cover day-to-day expenses?

Can the business meet its debt obligations on time?

Is there surplus cash available for reinvestment or expansion?

The insights provided by this statement are invaluable for making informed financial decisions, ensuring businesses can navigate challenges and seize opportunities without liquidity constraints.

Click to read the full blog regarding what is cash flow?

Breaking Down the Cash Flow Statement

1. Operating Activities: This section focuses on the core operations of a business—its day-to-day cash inflows and outflows. It reflects how much cash is generated or used by activities directly related to providing goods or services.

Examples of Cash Inflows:

- Revenue from sales.

- Payments received from customers.

Examples of Cash Outflows:

- Payments to suppliers for inventory or raw materials.

- Employee salaries and wages.

- Rent, utilities, and other operating expenses.

Illustrative Example:

Imagine a retail store generates $10,000 from sales in a month. During the same period, it incurs $7,000 in expenses such as payroll, rent, and utilities. The net cash flow from operating activities would be:

$10,000 (inflows) – $7,000 (outflows) = $3,000 (net cash inflow).

By analyzing this section, you can determine if the business’s operations are self-sustaining or require additional funding.

Examples of Cash Outflows:

- Purchasing new equipment, machinery, or property.

- Investing in other businesses or ventures.

Examples of Cash Inflows:

- Selling unused or outdated equipment.

- Proceeds from the sale of long-term investments.

While large investments may result in temporary negative cash flow, they often reflect a business’s commitment to growth and operational improvement.

Illustrative Example:

Consider a café that invests $1,500 in a new coffee machine. This transaction would appear as a negative cash flow in the investing activities section.

However, if the café later sells an old machine for $500, this inflow would offset part of the initial investment.

Examples of Cash Inflows:

- Loans or credit lines obtained from financial institutions.

- Proceeds from issuing shares or equity.

Examples of Cash Outflows:

- Repaying loans or principal amounts.

- Paying dividends to shareholders.

Illustrative Example:

A small business secures a $5,000 loan from a bank to expand its operations. Later, it repays $2,000 of the loan and $500 in interest. These transactions would be recorded as:

$5,000 inflow from financing activities.

$2,500 outflow (loan repayment + interest) under the same section.

A Practical Example: Piecing It All Together

Operating Activities: Sales revenue of $8,000 minus operating expenses of $4,000 results in a $4,000 net inflow.

Investing Activities: A $1,500 purchase of a new coffee machine results in a –$1,500 cash outflow.

Financing Activities: A $2,000 loan is taken, but $500 is paid in interest, resulting in a $1,500 net inflow.

By combining all three sections, the café’s total net cash flow is:

$4,000 (operating) – $1,500 (investing) + $1,500 (financing) = $4,000 increase in cash.

This final figure provides a comprehensive snapshot of the café’s cash position.

Why Regular Cash Flow Reviews Are Essential?

Identify Potential Cash Shortages: Early detection of cash flow gaps can help businesses plan and avoid financial strain.

Prepare for Future Expenses: Knowing how much cash is available allows for better budgeting and planning for upcoming bills or investments.

Ensure Financial Stability: Regular reviews help maintain a balance between inflows and outflows, preventing unexpected liquidity crises.

Common Challenges with Cash Flow Management

Overlooking Non-Cash Expenses: Depreciation and amortization don’t affect cash directly but can distort profit figures. Relying solely on profitability metrics without reviewing cash flow can lead to mismanagement.

Poor Expense Forecasting: Failing to anticipate upcoming costs can result in unexpected cash shortages.

Delayed Customer Payments: Late payments from customers can disrupt cash flow cycles, making it harder to meet financial obligations.

Pro Tips for Managing Your Cash Flow

Shorten Payment Cycles: Encourage customers to pay invoices promptly by offering incentives or implementing stricter payment terms.

Monitor Expenses Closely: Regularly review operating costs and identify areas for savings.

Maintain a Cash Reserve: Set aside emergency funds to cushion against unforeseen expenses.

Leverage Technology: Use accounting software like QuickBooks Online to track cash flow in real time.

Take Your Accounting Skills to the Next Level

This course is tailored for accountants, bookkeepers, and anyone looking to build a strong foundation in financial management. With practical examples, easy-to-follow lessons, and real-world applications, it’s the perfect way to enhance your skills and boost your confidence.

Don’t wait! Visit Accountutor.com today and transform your financial expertise.

Final Thoughts

The Cash Flow Statement is more than

just a financial document—it’s a roadmap to your business’s financial health.

By understanding and analyzing cash inflows and outflows, you can make smarter

decisions, plan for the future, and ensure the long-term success of your

business.

Whether you’re a seasoned accountant or a small business owner, mastering the Cash Flow Statement is an essential step toward achieving financial clarity. Start today, and take control of your cash flow like a pro.

Accounting and Bookkeeping courses for you

Subscribe to our newsletter

Policy Pages

Register for this webinar: How to Master QuickBooks Online— Without Feeling Overwhelmed